VAMP changes again: what merchants need to know

The recent updates surrounding the Visa Acquirer Monitoring Program (VAMP) have sparked plenty of debate and, frankly, a fair amount of confusion among merchants and industry professionals.

There are two key areas of uncertainty: While Visa has yet to confirm when the program will extend beyond Europe, Riskified has learned that a U.S. rollout is likely imminent. Additionally, Visa revised its initial announcement, clarifying that pre-disputes resolved via Verifi are now factored into the VAMP metric, eliminating the potential perceived game changer.

Understanding this evolving landscape is crucial for navigating fraud and dispute management effectively. Here’s what you need to know, including how things operated before VAMP, the initial changes Visa announced, and the most recent updates.

Network monitoring programs

Merchants are financially obligated to comply with the dispute and fraud monitoring programs established by Visa and Mastercard (whose two main programs are titled the Excessive Chargeback Program (ECP) and the Excessive Fraud Merchant (EFM) Program).

Visa and Mastercard also offer pre-dispute resolution tools provided by the companies, Verifi and Ethoca, respectively, which allow merchants to address disputes before they escalate into formal chargebacks. These tools allow merchants to be notified early, enabling them to proactively issue refunds or resolve issues, preventing a dispute from turning into a chargeback and impacting their dispute rate.

In parallel, issuers generate TC40 reports (Visa) and SAFE reports (Mastercard) whenever fraud incidents are detected. These reports provide valuable insights for acquirers to monitor fraud trends. Importantly, they are directly tied to network monitoring programs, as the fraud incidents recorded in these reports contribute to calculating a merchant’s fraud rate.

How things worked before VAMP

Before Visa introduced the updated VAMP, it had two compliance programs that monitored merchants’ monthly chargeback disputes and fraud risk:

- The Visa Dispute Monitoring Program (VDMP) tracked all chargebacks, including fraud and non-fraud. This standard threshold had a dispute-to-sales ratio of 0.9% and a volume of 100 chargebacks.

- The Visa Fraud Monitoring Program (VFMP) tracked fraud chargebacks and fraud alerts based on TC40 reports. This standard threshold had a ratio of 0.9% and under 75,000 USD in fraud volume.

Merchants who exceeded thresholds for fraud or disputes were flagged, fined, and sometimes questioned by Visa, incentivizing them to reduce these incidents.

Consolidation & exclusions under VAMP

In August 2024, Visa announced a new program, set to go into effect in April 2025, consolidating VFMP and VDMP under one program, VAMP, with a single new rate, determined by the count of disputes.

| VAMP rate |

| (# of fraud alerts + # non-fraud chargebacks) / (# of monthly transaction volume) |

| Acquirer portfolio level threshold | Merchant level threshold |

| ≥ 0.5% | ≥ 1.5% |

Visa’s initial announcement also included a significant, controversial change beyond the single new rate. Specifically, Visa planned to exclude pre-disputes resolved through Verifi’s Rapid Dispute Resolution (RDR) or the Cardholder Dispute Resolution Network (CDRN).

This exclusion had significant implications for the dispute resolution ecosystem, particularly for Mastercard’s Ethoca. The change would have disadvantaged Ethoca users since Visa would have still counted fraud alerts resolved using the platform against the VAMP rate.

From a competitive perspective, this change negatively impacted Ethoca and appeared designed to favor Verifi, Visa’s in-house solution. Mastercard and Ethoca, amongst other merchant advocates like the Merchant Risk Council (MRC), raised concerns about the anti-competitive nature of this policy, which they argued pressured merchants and acquirers to migrate to Visa’s tools.

Visa retracts the exclusion

In March 2025, Visa retracted the proposed exclusion. This means that fraud-related pre-disputes resolved through Verifi (alerts) are once again counted in the VAMP metric (no longer excluded). As always, pre-disputes that are not fraud-related and are resolved to prevent chargebacks will not be included in the metric.

Visa’s retraction has two key implications for merchants and acquirers:

- No artificial advantage for Verifi: By reversing its decision, Visa eliminated the artificial edge Verifi gained under the original proposal. This eliminates anti-competitive issues and removes unnecessary pressure on merchants to switch to Visa’s dispute resolution tools.

- Continued need for monitoring: Acquirers and merchants must account for all disputes and fraud alerts under the VAMP ratio, regardless of dispute resolution (Verifi or Ethoca). Proactive monitoring and early resolution remain critical for maintaining compliance under VAMP.

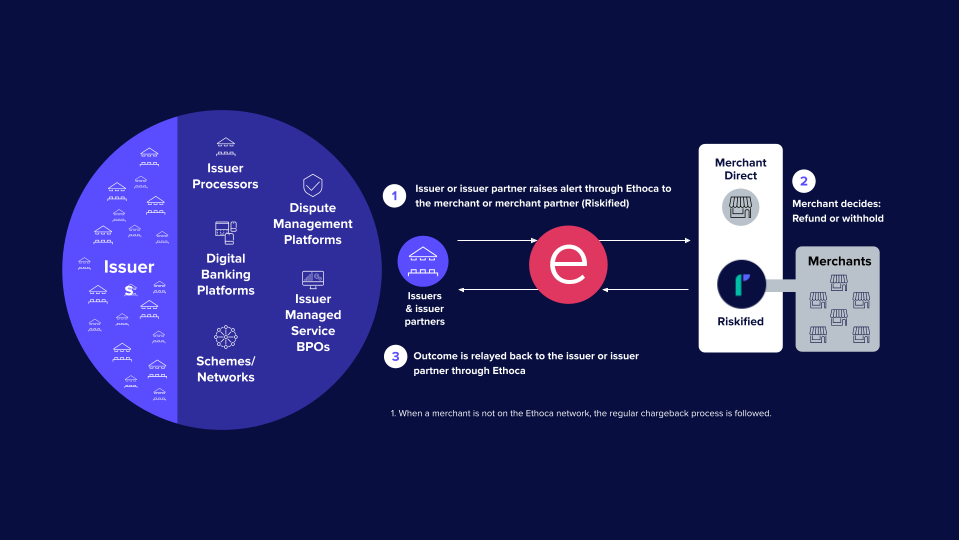

Ethoca’s role in the pre-dispute landscape

Amid the uncertainty surrounding VAMP, Ethoca remains central to merchants’ pre-dispute management efforts. Ethoca alerts allow merchants to identify disputes early, engage directly with customers, and resolve issues in ways that prevent chargebacks, saving merchants time, money, and reputational damage in the long run.

Riskified integrates Ethoca’s alerts into its Control Center dashboard, streamlining merchants’ ability to take decisive action on chargeback alerts. Ethoca’s tools remain one of the most effective options for reducing disputes and staying in compliance with Visa’s monitoring thresholds.

Ethoca Alerts: sharing actionable issuer information with merchants

What’s next for merchants

When Visa introduced VAMP, it was set to begin with a three-month formal advisory period starting April 1, 2025, but Visa has since shifted the enforcement timeline. The advisory phase will now extend to six months, with VAMP enforcement officially commencing on October 1, 2025, instead of the previously planned July 1, 2025.

The evolving nature of VAMP policies has left many merchants assessing how best to adapt. Ongoing tracking and monitoring of industry changes and updates remain essential for merchants to navigate these new rules.

Riskified is dedicated to supporting merchants by simplifying chargeback representment and offering clear, actionable guidance on VAMP compliance. We actively provide training to help merchants stay informed and prepared. For U.S.-based merchants, we’re focusing on equipping them with the tools and strategies needed to adapt should VAMP’s requirements extend beyond Europe, especially given the unique challenges of a market where 3DS isn’t yet a standard.

Continued need for fraud prevention

Clearly, it is important to remain proactive in managing disputes. Whether a chargeback stems from fraud or another issue (e.g., service-related), tools like those offered by Riskified, in partnership with Ethoca, enable merchants to address disputes swiftly and effectively.

That said, at Riskified, we believe preventing fraud is the most effective way to avoid reaching monitoring thresholds. And with Visa’s recent retraction eliminating any promised advantage of pre-dispute resolution, there is no real alternative for fraud prevention.

By staying informed, following clear VAMP compliance guidelines, and leveraging the right solutions, you can confidently navigate this complex landscape while keeping fraud prevention front and center. We’re here to help you every step of the way.